Photo credit: Cagdianao Mining Corporation

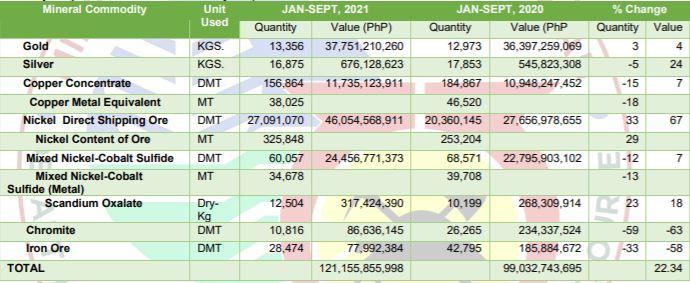

Metallic mineral production value sustained growth at 22.34% from PhP99.03 billion in January to September 2020 to PhP121.16 billion in January to September 2021, a difference of PhP22.12 billion.

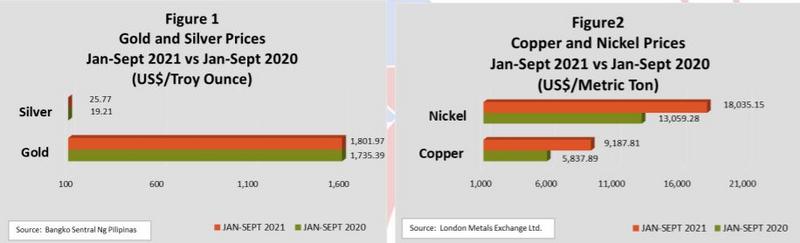

The strong metal price coupled with the better mine production of nickel ore during the review period was the vital factor for this development. Prices of leading metals gold, silver, copper, and nickel remained bullish, year-on-year. Precious metals gold and silver reported an average price of US$1,801.97 per troy ounce and US$25.77 per troy ounce from US$1,735.39 per troy ounce and US$19.21 per troy ounce, year-on-year, up by almost US$67 and US$7, respectively. In addition, the nine-month averages for copper and nickel stood tall at US$9,187.81 per metric ton and US$18,035.15 per metric ton, respectively. Copper price went up by 57% from US$5,837.89 per metric ton, while nickel enjoyed a 38% increase from US$13, 059.28 per metric ton.

In terms of percentage contribution to the country’s total production value, nickel with the aid of the other nickel by-products, mixed nickel-cobalt sulfide (MNCS) and scandium oxalate (ScOx) continued to outperform the others accounting for more than 58% or PhP70.83 billion. Lagging behind was gold with 31% or PhP37.75 billion, on its tail was copper with almost 10% or PhP11.74 billion. Finally, silver, chromite, and iron ore rounded up less than 1% or PhP0.84 billion. Over the recent years, with the advent of the production of nickel products (MNCS and ScOx) from the operations of Hydrometallurgical Processing Plants Coral Bay Nickel Corporation and Taganito HPAL Corporation, the gap in the contribution between gold and nickel ore with nickel products continued to widen. It was in 2018 when nickel ore & nickel by-products first exceeded gold as the prime contributor in overall, metallic production value.

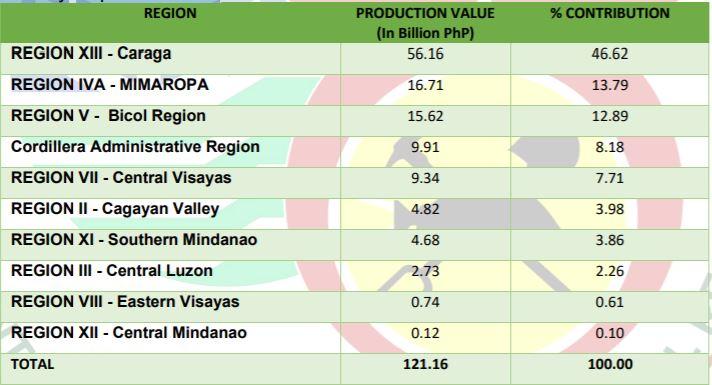

In terms of distribution of Regional production value, Caraga Region had the lion's share with 46.62%, followed by MIMAROPA with 13.79%, and in third was Bicol Region with 12.89%. In terms of the number of operating metallic mines in the Regions. Caraga headed the pack, with two gold mines, one chromite mine, 18 nickel mines, one hydrometallurgical processing plant, and one gold processing plant.

Nickel direct shipping ore together with its by-products MNCS and scandium oxalate remained true to form, as it displayed dominance over other metals. Production value went up from PhP50.72 billion to PhP70.83 billion, an almost 40% or PhP20.11 billion increase. Production volume and value of nickel direct shipping ore recorded 29% and 67%, respectively from 253,204 metric tons with an estimated value of PhP27.66 billion to 325,848 metric tons with an estimated value of PhP46.05 billion year-on-year. Breaking it down further, in terms of mine regional production Caraga Region the nickel capital hub of the Philippines accounted for 76% with 248,001 metric tons, followed by MIMAROPA with 17% or 54,936 metric tons while Regions III and VIII accounted for 6% or 18,939 metric tons and 1% or 3,971 metric tons, respectively. Emir Mineral Resources Corporation located at Guiuan, Eastern Samar is the latest addition to the roster of producing nickel mines in the country. Moreover, the production volume and value of ScOx, a by-product in the operation of Taganito THPAL recorded a production volume and value of 12,504 dry-kilograms with an estimated value of PhP0.32 billion, a 23% and 18% growth from its previous 10,199 dry-kilograms with an estimated value of PhP0.27 billion, year-on-year. On the other hand, MNCS performance was diverse as production volume declined by 13% from 39,708 metric tons to 34,678 metric tons, year-on-year. Production value, however, rose by 7% from PhP22.80 billion to PhP24.46 billion.

Performance of the yellow metal remained consistent with production volume and value demonstrating positive movement from 12,973 kilograms with an estimated value of PhP36.40 billion to 13,356 kilograms with an estimated value of PhP37.75 billion, up by 384 kilograms and PhP1.35 billion, respectively. In terms of mine output, Bicol Region held the rein with 40.89% or 5,462 kilograms of the country’s gold production. Philippine Gold Processing and Refining Corporation and Joshon Mining Corporation are the current gold mines in the region. Cordillera Administrative Region was in far second accounting for 15.10% or 2,017 kilograms. Said region has three gold mines, Lepanto Consolidated Mining Corporation, Benguet Corporation –Acupan Contract Mining Project, ItogonSuyoc Mines, Inc., and 10 approved Minahang Bayan. Out of the 10 MB only Loacan Itogon Pocket Miners Association reported production. CAR was closely followed by Caraga with 14.91% or 1,991 kilograms. Said Region has two gold mines, Philsaga Mining Corporation (PMC) and Greenstone Resources Corporation (GRC). Only PMC recorded production, GRC is still under Care & Maintenance status. Other regions with gold mines include II, XI, VII, and XII.

Overall silver production volume, dip by 5% from 17,853 kilograms to 16,875 kilograms year-on-year. While production value grew by 24% from PhP0.54 billion to PhP0.68 billion. The substantial PhP0.13 billion rise in value despite the 978 kilograms shortfall in volume was due to the upbeat silver price from US$19.21 per troy ounce to US$25.77 per troy ounce year-on-year, up by US$6.55.

For copper production, we saw copper volume slip by 18% from 46,520 metric tons to 38,025 metric tons, down by 8,945 metric tons both Philex Mining Corporation and Carmen Copper Corporation incurred deficit. The production value on the other hand enjoyed a 7% increase from PhP10.95 billion to PhP11.74 billion, year-on-year, up by PhP0.79 billion. The bullish metal price during the period made this possible. Another optimistic development is the renewal of the Financial or Technical Assistance Agreement of OceanaGold (Phils) Inc. last July 2021, its re-entry to the production stream will naturally boost not only copper but also gold and silver output. Noteworthy, in August 2021 OGPI reported a total sales for gold and silver amounting to PhP105.86 million bound to Australia. The ore sold came from their inventory.

On the iron ore production, only Leyte Ironsand Project of MacArthur Iron Projects Corp/Strongbuilt Mining & Development Corp. reported production with 28,474 dry metric tons with an estimated value of PhP77.99 million. Same period last year Atro Mining Vitali Iron Inc. was the sole producer.

On chromite production, volume and value went down by 59% and 63% from 26,265 dry metric tons with an estimated value of PhP234.34 million to 10,816 dry metric tons with an estimated value of PhP86.64 million year-on-year. Only Techiron Resources Inc. reported production.

For each commodity, the frontrunners in terms of mine production were:

On the local front, the passage of critical and long overdue policies has created an optimistic buzz in the minerals sector. Such policies include:

- DAO 2021-12 (Guidelines for the Automatic Renewal of the Exploration Period and the Timely Filing of Declaration of Mining Project Feasibility Under the Exploration Permit, MPSA, FTAA, and Similar Mining Tenements);

- EO 130 (Amending Section 4 of Executive No. 79, S. 2012, Institutionalizing and Implementing Reforms in the Philippine Mining Sector, Providing Policies and Guidelines to Ensure Environmental Protection and Responsible Mining in the Utilization of Mineral Resources);

- DAO 2021-25 (Implementing Rules and Regulations of Executive Order No. 130, Amending Section 4 of EO No. 79, S. 2012). Major features of the DAO include: (1) Lifting of the moratorium in the acceptance of applications for Mineral Agreement pursuant to DAO No. 2010-21; (2) Approved DMPF under the EP may now mature into Mineral Agreement subject to compliance with certain requirements; and (3) Paved way for the review of the pro-forma MPSA and renegotiation of existing ones.; and

- DAO 2021-29 (Extended Application Period for the Disposition of Residual Stockpiles) the application period for the disposition of residual stockpiles sourced from small-scale mining operation previously covered by valid mining permits is extended until 31 December 2022.

It is important to highlight that out of the total land area of the Philippines of 30 million hectares, the total area covered by mining tenements as of 31 October 2021 is only 745,685.48 hectares or 2.48%. This only pertains to the permits issued by the national government and does not include the permits issued by the local government. Moreover, with the EO 130, the government can now approve Mineral Agreements. To date, there are 313 approved Mineral Production Sharing Agreements with a total land area of about 576,482.65 hectares. It should be emphasized that said area is still subject to the mandatory relinquishment by contractors as provided by law.

In addition, the MGB is working diligently on the formalization and declaration of the new Minahang Bayan. At this time, 43 MB was already been declared all over the country with 170 pending applications. Among the declared Minahang Bayan, there are 13 under the Luzon area, 3 in Visayas, and 27 in Mindanao. For metallic minerals, commodities will be limited only to gold, silver, and chromite and shall have a term of two years, renewable for like periods but not to exceed a total term of six years. With MB very much in the scene, we are optimistic that gold, silver, and chromite production will rise.

Article courtesy of the Mines and Geosciences Bureau